Credit Report Search | Finding Your Report Online

November 7, 2024

Unlocking Your Financial Future: A Guide to Credit Reports

Introduction: Your Financial Fingerprint

Imagine your credit report as a personalized summary of your financial dealings. It's like a snapshot of your borrowing and repayment history, showing lenders your track record. Understanding it is key to getting the best deals and achieving your financial goals. This guide will help you navigate this crucial document.

Understanding Your Credit Report

What Exactly is a Credit Report?

Source: tasdeeq.com

A credit report details your borrowing history, showing if you pay bills on time, any missed payments or delinquencies, and any other relevant information like accounts opened or closed. It's important! Think of it like a history book of your financial transactions.

Source: nerdwallet.com

Why is it Important?

It helps you identify areas needing improvement and understand the financial picture. Lenders see it and determine how likely you are to repay loans. "A good credit report opens doors!"

What Does it Show?

- Payment history (key!)

- Amounts owed

- Types of credit used

- Length of credit history

Why Should You Care?

It lets you track your financial habits. Good credit helps in many ways like low interest rates on loans and better lease terms on apartments! This knowledge gives you strength!

Getting Started: Accessing Your Report

How to Obtain a Free Copy

Getting a copy is pretty simple! Check if a site offers this service. Some are free; it depends! Check reputable sites to download your credit report for free; they usually come up as 'free credit report download', or maybe with a few other terms attached.

Helpful Hints:

- Search for websites specializing in credit reports.

- Check official websites; government agencies usually do that job well!

- Check different organizations if you aren't sure.

- Don't get it from random emails; those are probably scammers.

(Be super careful who you get this from. There are people out there who want to trick you!)

Why Different Organizations?

Credit reports can vary slightly among different bureaus or credit rating companies like Experian and TransUnion, because they all maintain information about credit from different locations. Be wise and seek your report at various organizations (different websites), because all give different results and info sometimes. (Just to ensure there's no issue in any location, make a double or triple-check of reports from these various sites! You need to feel secure.)

Checking Regularly: A Key Habit

Keep an eye on your credit report to spot mistakes or inconsistencies early. "Early detection saves trouble!" You're strong if you always pay attention to your report. Check frequently (annually at least!). You have an important tool to do just that. (Being cautious and taking care will allow you to avoid much grief!)

Checking for Mistakes

If there's any inaccurate data, immediately report it. ("Don't let wrong things affect your financial record.")

- Incorrect accounts, for example, showing loans you did not receive or not recorded yet

- Missing transactions

- Inaccurate payment history data

(Fix issues promptly because a little mistake may be huge for future financial deals!)

Interpreting Your Credit Report: What to Look For

Understanding Scores

Your credit score is a number (usually between 300-850) which reflects how reliable you are with managing money and your finances. A good score typically improves opportunities like housing and credit card offers. Higher numbers are always better. ("Credit scoring, is a way of measuring a person's financial reliability or risk.")

Source: credit.com

Sections within your Credit report

Here are examples from the main section details. They give many other important items of detail to look at, too! These can sometimes be hard for some to digest.

(But understanding your information from different parts is vital to know what your standing is.!)

- Payment history: Note late payments, defaults (that could have come with negative outcomes on a credit history!), account delinquency, which means being late on payments! Pay promptly, is the solution!

- Amounts owed (current credit amount/debt in total): How much you currently owe on different credit lines. It gives a clear idea of overall financial commitments.

- Types of Credit Used: Overview of loan kinds you have like mortgages or auto loans, also other loans such as credit cards and installment payments are important. They are crucial as they show various kinds of financial management ability and practices!

- Length of credit history: The entire span of how much you have established credit over your lifetime. Many creditors like having individuals or families with a lot of consistent history.

(Note, however, these are just part of it. Different sections might have varying aspects of this section depending on where or when the report was run! All in all, this gives the report context, but don't just look at individual parts; view the overall and bigger picture! It helps in evaluating your financial picture much better. It gives more details if the reports had different data at various sites.)

Protecting Your Credit

:max_bytes(150000):strip_icc()/GettyImages-1002493636-cfdb52fdc897411ca1ab7e1e9c2ddcc4.jpg)

Source: investopedia.com

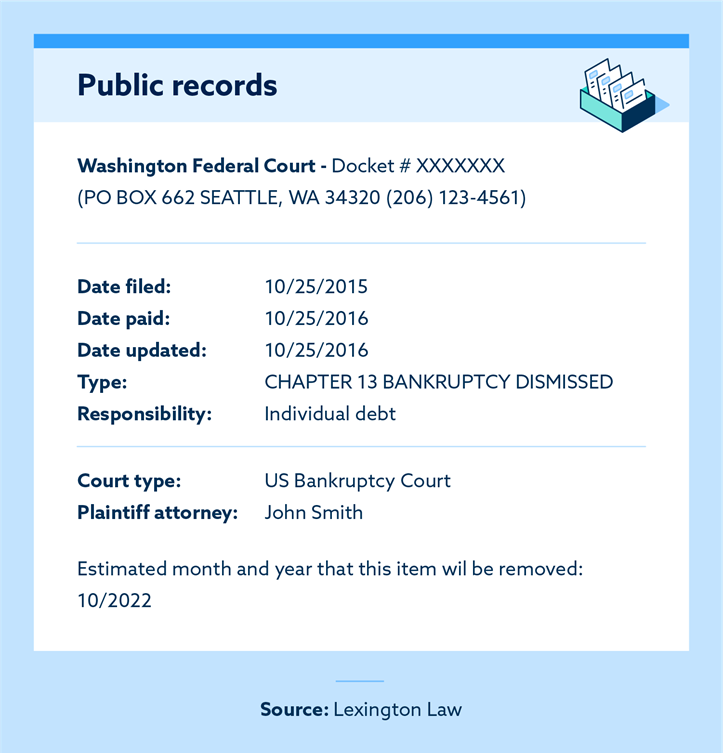

Identity Theft: A Real Threat

Source: lexingtonlaw.com

Keep your accounts safe. Protect yourself from theft by safeguarding personal and financial details like usernames, passwords, credit/debit cards, and even emails. Be smart about how you disclose financial data online; do not make it easy for anyone to access sensitive details on your computer or mobile device.

Building Good Credit: The Takeaway

Small acts like paying on time (a very critical point) builds a fantastic history that's rewarding. Take part and actively track your financial activity as you continue this endeavor for better financial health!

Actionable Steps Summary:

- Obtain a free credit report regularly (at least once a year).

- Identify any errors and promptly dispute inaccurate information.

- Maintain on-time payments across all credit accounts to increase your positive credit history score.

Conclusion: You Got This

You've started understanding how important it is to review credit history! Credit reporting is important because, well, credit! Maintaining excellent credit practices improves your options and reduces interest rates when it comes to important issues such as a mortgage or loan! Always use sound and solid financial steps that aid you to take great action on building a credit history.

(Be sure that your financial wellbeing will always improve through wise credit practices!)

Further Learning: