Experian Credit Education | Learn About Your Credit Score

October 7, 2024

Experian Credit Education | Learn About Your Credit Score

Understanding Your Credit Score: It's More Than Just a Number

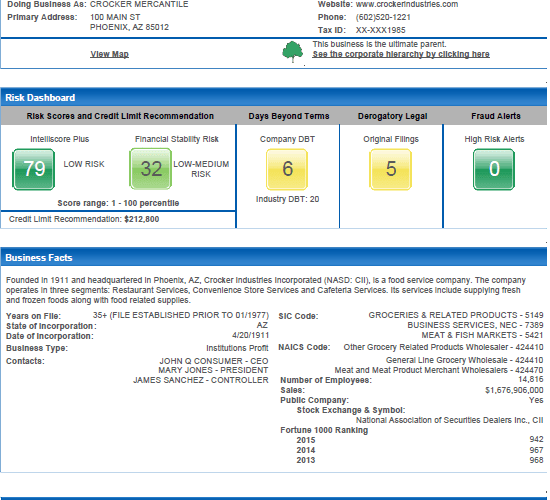

Source: nacmconnect.org

Your credit score is a little like a report card for your borrowing habits. It shows lenders how responsible you are with money. This report, based on your past behavior, helps them decide if you're a good risk to lend money to. It gives you a snapshot of your financial health.

What is a Credit Score?

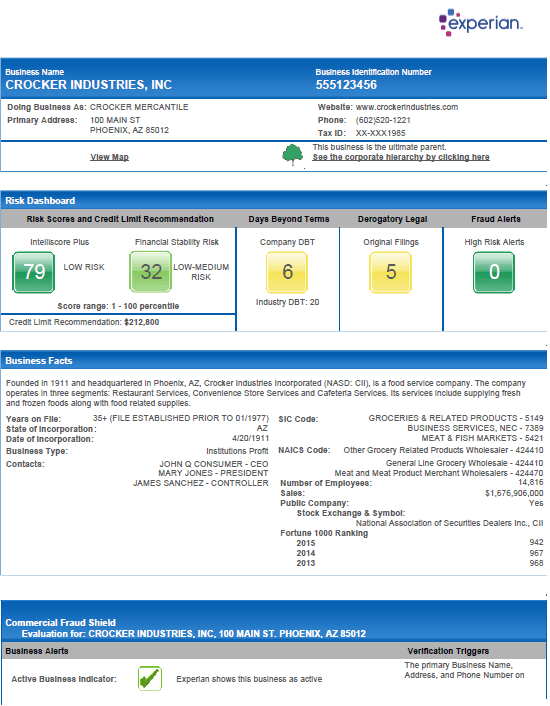

Source: mzstatic.com

A credit score is a three-digit number that summarizes your credit history. Think of it as a snapshot of your borrowing behavior. Lenders use this number to decide how likely you are to repay a loan.

Factors that Affect Your Score:

- Payment history: Paying bills on time is super important. Late payments hurt your score.

- Amounts owed: How much debt do you have? High debt can mean a lower score.

- Length of credit history: The longer you've had credit accounts, the better it looks.

- New credit: Applying for many new credit cards quickly might hurt your score. It shows you're taking on more debt.

- Types of credit: Having a mix of different types of credit (like a credit card and a loan) can be good.

Why is My Credit Score Important?

Your credit score is crucial for getting things like:

- Loans for a car or a house

- Credit cards

- Apartment rentals

Source: experian.com

A high score is like having a good reputation with lenders.

How Does Your Score Work?

Think of it like this:

- A higher score means you are a more reliable borrower. It shows you're good with money.

- A lower score means lenders might be more cautious.

It's all about your track record with repaying what you owe. It builds over time, based on your past behavior.

Building a Good Credit Score:

It's not rocket science! Start now and get a head start on building a good one:

- Pay bills on time: This is the most important thing! "Punctuality is the politeness of kings."

- Keep your credit card balances low: Don't let them get too high!

- Apply for new credit accounts cautiously: Don't open too many accounts at once.

- Check your credit report regularly: Knowing where you stand is key. Your report is like a mirror reflecting your creditworthiness.

- Don't close unused accounts: Keeping old accounts open for a while can boost your score.

Understanding Your Credit Report

Your credit report is a detailed record of your credit accounts. It's like a complete history book showing everything from credit cards to loans.

What's in Your Credit Report?

- Your personal information, like your name, address, and social security number

- All your credit accounts and your activity on them. Like payment history.

- Your inquiries (requests for credit).

"A good reputation is more valuable than gold."

Your Credit Report is Like a Mirror:

(It shows you how responsible you are with borrowed money)

How to Check Your Credit Report

Checking your credit report is like taking a look in the mirror, it allows you to see where you stand…

- You can get free copies from annualcreditreport.com

- Check regularly (at least once a year)

Credit Myths Debunked

Let's tackle some common misconceptions about credit scores:

Myth 1: A bad credit score means you'll never get approved for anything.

(Reality:) It might make it harder, but it's not impossible. There are ways to improve your score!

Myth 2: Having no credit history means a terrible score.

(Reality:) It's like starting a new report card—you don't have any grades yet, but you can build it by taking on responsible credit and paying your bills on time.)

Myth 3: My credit score only affects my credit card applications.

(Reality:) Your score affects your ability to get a loan for a car, a house, or even an apartment. It's a big part of your financial picture.)

What If Your Credit Score Is Low?

Don't despair! A low score isn't the end of the world. Focus on fixing the issues on your report. It's like taking steps to improve a low grade.

Steps to Take:

- Pay bills on time.

- Keep credit card balances low.

- Check your report regularly.

- Ask for help if needed! There are resources available to give advice and support you.

Questions You Might Have:

-

What happens if I don't know how to manage my credit?

- Seek advice from knowledgeable people (family, mentors) or use resources from financial institutions.

-

How can I avoid credit problems in the future?

- Carefully consider the terms of any credit agreements before you sign. Be smart with borrowed money.

-

What can I do if I'm having trouble paying my debts?

- Contact your creditors and negotiate payment plans. This will help prevent damage to your credit score. Don't give up!

Source: redd.it

Building a Positive Credit History:

Making smart choices with your money now can pay off later (in many ways).

Tips:

- Don't take on more debt than you can comfortably handle.

- Build a solid savings routine. Saving is a sign of good financial habits. It's like preparing for the future.

- Pay your bills on time. "A stitch in time saves nine."

Resources for Further Learning

- Experian's website

- Local credit counseling agencies

- Consumer financial protection agencies

It's like learning how to ride a bicycle – at first, it might be a little tricky, but with practice, you'll get the hang of it!

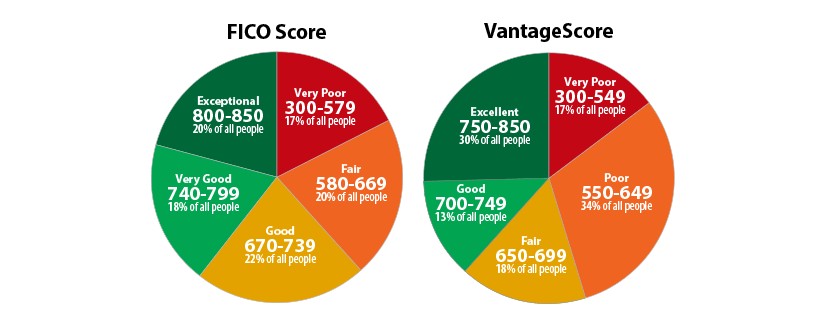

Table: Understanding Credit Scores

| Score Range | Meaning |

|---|---|

| 700-850 | Excellent, low risk |

| 650-699 | Good, moderate risk |

| 550-649 | Fair, higher risk |

| Below 550 | Poor, very high risk |

Remember, building a good credit score is an ongoing process. It's like growing a garden – it takes time and effort, but the rewards are worth it. Be responsible with credit, and your future financial opportunities will be brighter.