Experian Home Page | Exploring the Official Website’s Features

October 13, 2024

Experian: Your Credit Score, Explained (and a Bit More)

Hey, Friend! Let's Talk Credit

Source: security.org

Ever feel like credit scores are some secret code? Like they're written in a language only financial gurus understand? Don't worry, you're not alone! I'm here to break it down. This site, Experian, well, they help us make sense of it all.

Source: wixstatic.com

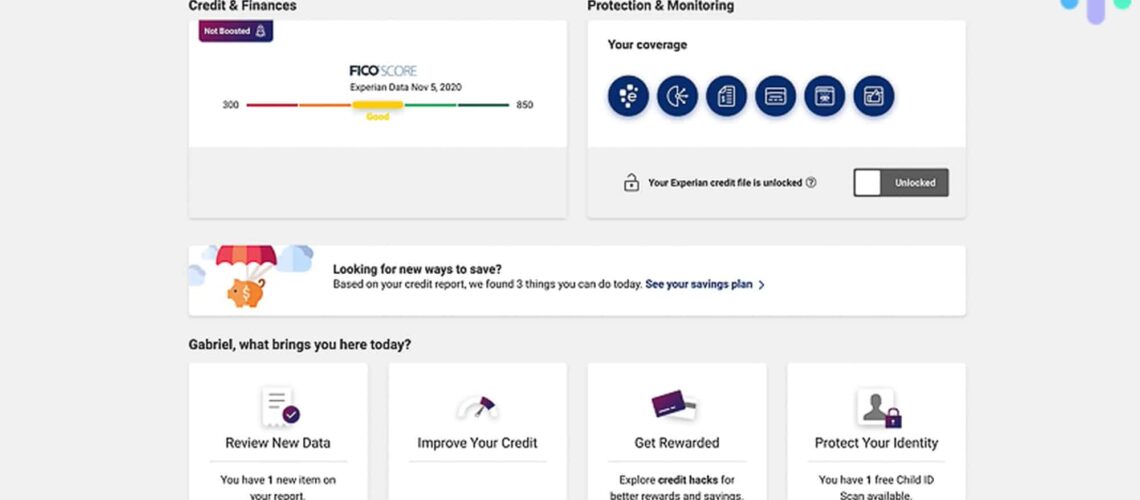

What Is Experian?

Experian is like the credit score report king, if there was such a thing! (Okay, maybe not king, but important, right?) They collect data about your spending and borrowing habits. This data makes up your credit profile, essentially your financial history report.

Simple Explanation

Source: mzstatic.com

Think of it like this:

- You use a credit card.

- Your actions (paying on time, or not, borrowing money, etc) leave a mark.

- Experian is the scorekeeper, keeping track of these actions.

So, Why Experian?

- Tracking your borrowing helps banks understand your creditworthiness.

- This helps you get a good deal.

- It’s all in your interest! Understanding your credit history helps you know if your plan for borrowing is going to succeed.

Source: idstrong.com

The Credit Report Decoded: Inside the Details

The Building Blocks: What's In A Report?

Let's face it. Credit reports look confusing, right? They have all this numbers and texts and columns (so, many things!) But each little part tells a story.

- Payment History: How well (or badly!) you paid off your past dues and debt shows whether you were reliable in the past.

- Amounts Owed: This measures how much you have borrowed versus what you can comfortably pay back. Important details in loan history (payments done on time or late payments).

- Length of Credit History: The longer you use credit, the more trustworthy (stable, better paying customer) you appear. Wow! That was really simple!

- New Credit: Applying for a loan (even if it doesn't become a loan eventually) has an impact. Experian needs to understand why someone is applying (so they see you're being a responsible citizen! 😀 ) .

- Types of Credit: Do you have multiple types (or varieties)? Having various kinds of borrowing activities like mortgages, personal loans, etc. adds dimension.

Important Question for the Future : Will credit reports have an impact on your insurance costs?

Possibly! But they haven’t been connected just yet. The future of insurance in terms of credit ratings is yet unknown.

What Makes Your Score?

This might sound complicated but this is how it's often done:

<br>

| Category | Percentage | Importance |

|---|---|---|

| Payment History | 35% | This is the BIGGEST factor! Paying on time consistently and shows how you respect payments. |

| Amounts Owed | 30% | The less debt you have compared to your income and ability to pay off debts influences your rating. |

| Length of History | 15% | A long credit history generally means a higher chance of your ability to consistently meet debts and payments. |

| New Credit | 10% | Too much recent borrowing suggests increased risk and will not influence as much for the time being |

| Types of Credit | 10% | A combination of varying and relevant borrowing activities strengthens your reputation as a reliable person to do business with. |

Example

- Paying your bills on time each and every month, a history that reflects this positive characteristic.

- A moderate debt-to-income ratio and avoiding high balances or late payment.

Source: wecantrack.com

Personal Experiences

(This is me, adding some thoughts…)

As someone exploring all the details on my own Experian account, one significant thing to remember: Your financial story matters to yourself, others, the world (hopefully) as well! Every payment shows responsibility, showing banks and financial services how reliable a consumer you are!

Credit Scoring, Beyond the Numbers

Understanding Your Credit Profile

Having good credit has the great reward for loan deals and lower costs overall.

A low score can often come down to small aspects of your record and past, not even something in your immediate control today.

Understanding these impacts, it is important to:

- Understand your score

- Look for early errors.

- Work on areas you are worried about fixing or dealing with.

Your Financial Roadmap

Credit scores are vital for obtaining loans, apartments, and so on. These help predict whether you might make a suitable long-term renter, responsible borrower or whether any problems exist before engaging you into further interactions.

Practical Actions:

What steps are required in managing your credit scores effectively?

- Review your reports regularly for any potential discrepancies.

- Dispute any inaccurate items reported (so you avoid bad records being present).

- Aim for long-term stability as opposed to short-term strategies that will not create long-term benefits or effects in the end.

Taking Control: Tips for a Healthy Credit Score

These things (listed) could have implications later, it is beneficial to work hard today so future problems can be managed well!

- Set a Budget: You can budget by tracking spending, figuring out what's crucial to keep for necessities, then using savings (as savings build).

- Avoid Overspending: Spending over what you can repay shows carelessness! Don't let things you enjoy outweigh what you can sustainably keep spending each month to avoid trouble. Remember the adage, "Money is earned, but earned money has to be carefully handled"! (Not just for debt but to build long-term benefits).

- Keep Existing Accounts Active: You have loans (maybe from years back) keep those active as opposed to immediately paying off and closing things right now, unless it will be in better circumstances!

- Build Up Your Payment History: Try building credit now.

Remember:

Paying your bills on time (always!). Paying more each month, to clear balances (but also keep payments as well as a history of regular on time paying on credit!).

Final Thoughts: What Next?

Experian isn't just some faceless company. They give people power by showing financial history records, which hopefully you can use and learn about!

This journey (of personal financial growth and understanding) involves steps, questions, decisions, actions and reviews for your overall future growth and comfort.

Let me know if you need clarification or more insights. What about you – any financial insights you might have that's helpful and a part of your financial routine, strategy and journey (experiences?) It helps me personally.