Log in to Experian Account | Manage Your Credit Report

October 7, 2024

Your Credit Report: A Look Inside Your Financial Story

This article will help you understand your credit report, a super important document that shows your borrowing history. It's like a report card for your financial life!

What is a Credit Report?

Source: experian.com

Imagine your financial history is written down in a detailed report. This is your credit report. It shows lenders how you've handled borrowing in the past… things like paying back loans, credit cards, and other debts. Lenders use this to decide if they want to lend you money.

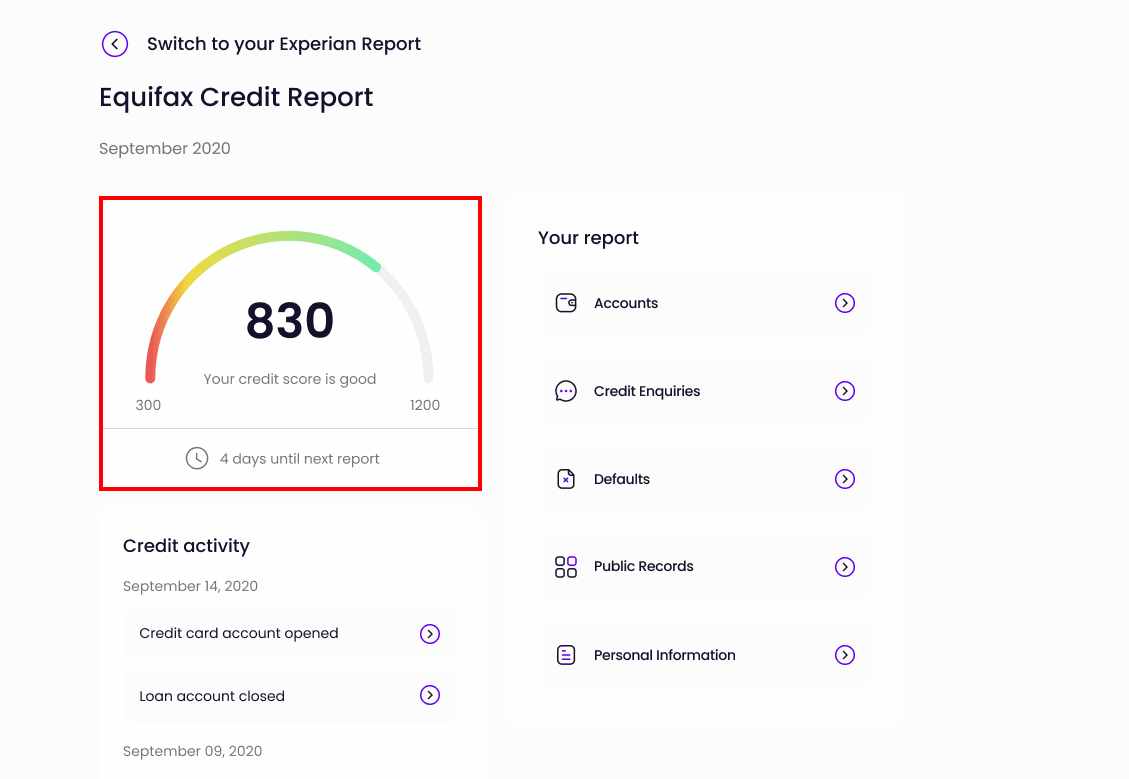

Source: com.au

Why is it Important?

Your credit report is crucial for getting loans, credit cards, and even apartments! A good report helps you get better deals and rates! It's like a letter of recommendation for your financial trustworthiness.

What's Inside Your Credit Report?

Your credit report has lots of information about your borrowing. Here's a breakdown:

- Personal Information: Your name, address, and Social Security number (this is important to protect your privacy).

- Credit Accounts: This shows your credit cards, loans, and any other accounts you have. This includes payment history, credit limits, and the current balance.

- Payment History: Lenders see if you've paid your bills on time. Being on time is really important!

- Credit Inquiries: If you applied for a loan or credit card, this will be noted. This shows how many times you've asked for credit.

Understanding the Different Sections

Payment History

- On Time: Paying bills on time is like getting good grades, and you want to maintain a good payment history!

- Late Payments: Late payments can affect your credit score. It's like getting a bad grade… it might hurt your chance of getting a loan. But it's not the end of the world! You can improve your score.

- Delinquent Accounts: If you can't pay your bills, this section shows lenders you have problems. It's important to try to catch up on these if you can.

Credit History

- Types of Credit: This tells lenders the types of credit accounts you have, like credit cards or loans.

- Credit Utilization: This is how much debt you have compared to your credit limits (the total amount you can borrow). Keep your credit utilization rate low (try to keep it under 30%).

Credit Inquiries

- New Credit Applications: Lenders look to see how many times you've applied for credit in a short time. Too many applications can hurt your credit score.

Credit Mix

Source: experian.com

- Different Credit Accounts: Having a mix of credit accounts (like credit cards and loans) can help. A diverse credit history is seen as more trustworthy.

Credit Scores: Your Financial Grade

Your credit score is a number that lenders use to evaluate your trustworthiness when it comes to borrowing. A high credit score means you're a low risk, so you might get better loan rates and terms… a higher score is great!

How is a Credit Score Calculated?

Your credit score is a complicated calculation based on many factors, including:

- Payment History: On-time payments are super important.

- Amounts Owed: How much debt you have compared to your available credit.

- Length of Credit History: The longer you've had credit accounts, the better.

- Credit Mix: Having different types of credit accounts helps.

- New Credit Inquiries: Less inquiries are better!

What's a Good Credit Score?

A good credit score typically ranges from 670 and up. A high credit score will help you get loans, cars, and apartments more easily!

Improving Your Credit Report

Improving your credit score takes time… but it's definitely worth it!

- Pay Your Bills on Time: This is the most important part! Being on time builds your good credit history.

- Keep Your Credit Utilization Low: Don't use too much of your available credit.

- Don't Apply for Too Much Credit: Think before applying for multiple loans or credit cards.

- Monitor Your Credit Report: Check your credit report regularly.

- Review Your Accounts: Make sure all the information on your report is accurate and up to date.

Frequently Asked Questions

Q: What if I see something wrong on my credit report?

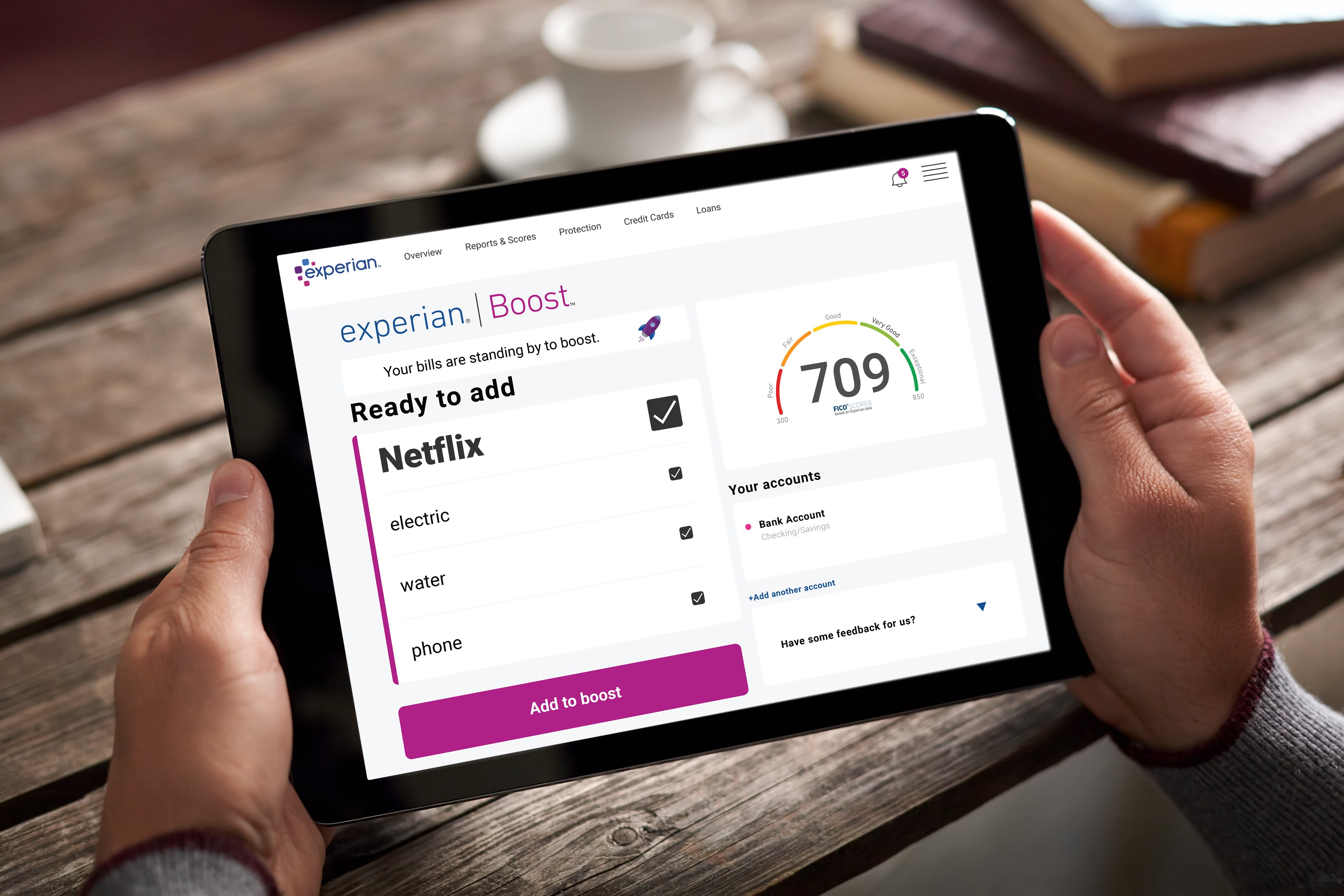

Source: boardingarea.com

A: You can dispute incorrect information! If you see something inaccurate, contact Experian, or another credit reporting agency (Equifax or TransUnion), and explain why it is wrong.

Q: How often should I check my credit report?

A: It's a good idea to check your credit report at least once a year to make sure everything is accurate.

Important Reminders

- Privacy is Key: Protecting your personal information is super important!

- Financial Responsibility: Making smart financial decisions now will help you in the future. Wise financial choices matter.

- Don't Give Out Personal Information to Strangers: Protect your financial information from fraud.

Credit Reporting Agencies (CRAs)

- Experian: A major credit reporting agency.

- Equifax: Another major credit reporting agency.

- TransUnion: Another important credit reporting agency.

Credit Myths Busted!

- Myth: You can't improve your credit once it's damaged. (False!) You can work on it and improve it!

- Myth: A high credit score is the only thing that matters. (False!) It's important, but it isn't the end-all-be-all.

- Myth: Credit reports are only for getting loans. (False!) They're used for apartments and other things too!

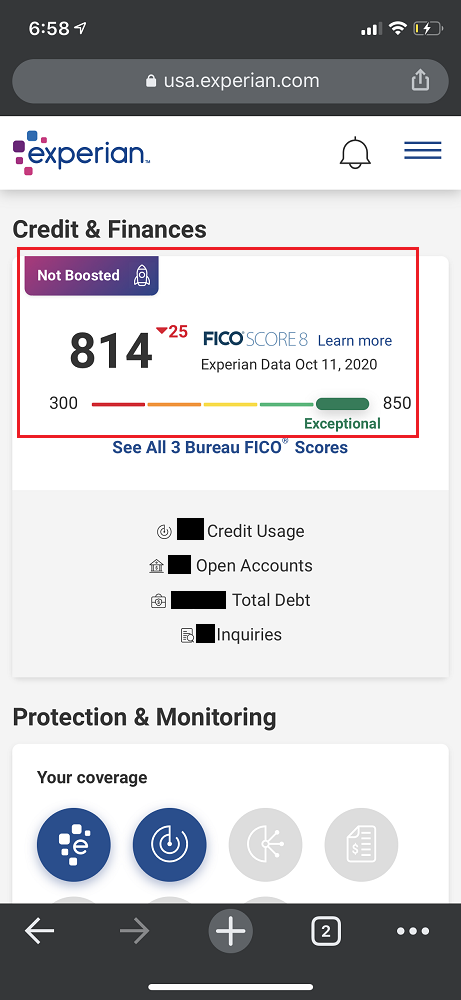

Source: cnbcfm.com

Conclusion

Your credit report is a significant part of your financial journey! It's like a map showing where you are financially. By understanding your credit report and how it works, you can make smart decisions and build a better financial future. "The key is to learn from your past and make informed decisions moving forward."

(This article is for informational purposes only and does not constitute financial advice.)