Log In to Experian Account | Secure Credit Report Access

October 7, 2024

Your Credit Report: A Super Important Guide

This article helps you understand your credit report, what it is, and how it works. It's like a report card for your borrowing, showing lenders if you're a good person to loan money to. Think of it as your borrowing history.

What's a Credit Report?

Imagine a special file, a sort of "credit history report," that lenders look at when you want a loan, like for a house or a car. This file is your credit report. It shows lenders how responsible you are with paying back money you borrow.

What's Inside Your Credit Report?

Source: krebsonsecurity.com

Your credit report is packed with information about your borrowing habits. It includes:

- Your personal information: Your name, address, Social Security number.

- Your credit accounts: Information about all the loans, credit cards, and other debts you have.

- Your payment history: Did you pay your bills on time? Are there any late payments?

- Credit inquiries: How many times have you applied for credit recently?

- Types of credit you have: Different types of loans or credit cards.

- Length of your credit history: How long have you been borrowing money responsibly? This helps lenders understand your habits over time.

Why is a Credit Report Important?

Your credit report is a key to getting loans and credit. Lenders use it to decide if they want to give you a loan or credit card. It's like a sign to lenders saying, "This person is responsible, or they aren't." You want to show them the good side of you!

Example of a Good Credit Report

- On-time payments on all accounts

- Low debt-to-income ratio (not owing too much compared to what you earn)

- Multiple open credit accounts (but not too many)

- History of borrowing and paying it back successfully

Example of a Not-So-Good Credit Report

- Lots of late payments

- High debt-to-income ratio

- Hard credit inquiries frequently

- Few open credit accounts (or none at all)

How to Access Your Credit Report

You can usually get a free copy of your credit report from each of the major credit bureaus. These are like the big record keepers. They are called Experian, Equifax, and TransUnion. (They're like the keepers of the credit file.)

How to Get Your Free Credit Report:

Source: experiancs.com

- Go to the websites of the three major credit bureaus listed above.

- Fill out the forms with your personal details.

- Pay close attention to any questions they might have, as they help them figure out who you are.

- Download or print out your report. (Keep a copy for yourself).

Understanding Your Credit Report

Your credit report is like a window into your financial history. It's a record of how you've handled credit in the past. It shows lenders what kind of borrower you are. ("History repeats itself," they say.)

Common Credit Terms You Might See:

- Credit score: A number (usually between 300 and 850) that shows how likely you are to pay back borrowed money. A higher score means a lower risk to lenders.

- Credit limit: The maximum amount of money you can borrow on a credit card.

- Credit utilization: The percentage of your available credit you're currently using. You want to keep this low (ideally under 30%).

Improving Your Credit Report: Steps You Can Take

You can't change your past, but you can definitely make your future credit report look better.

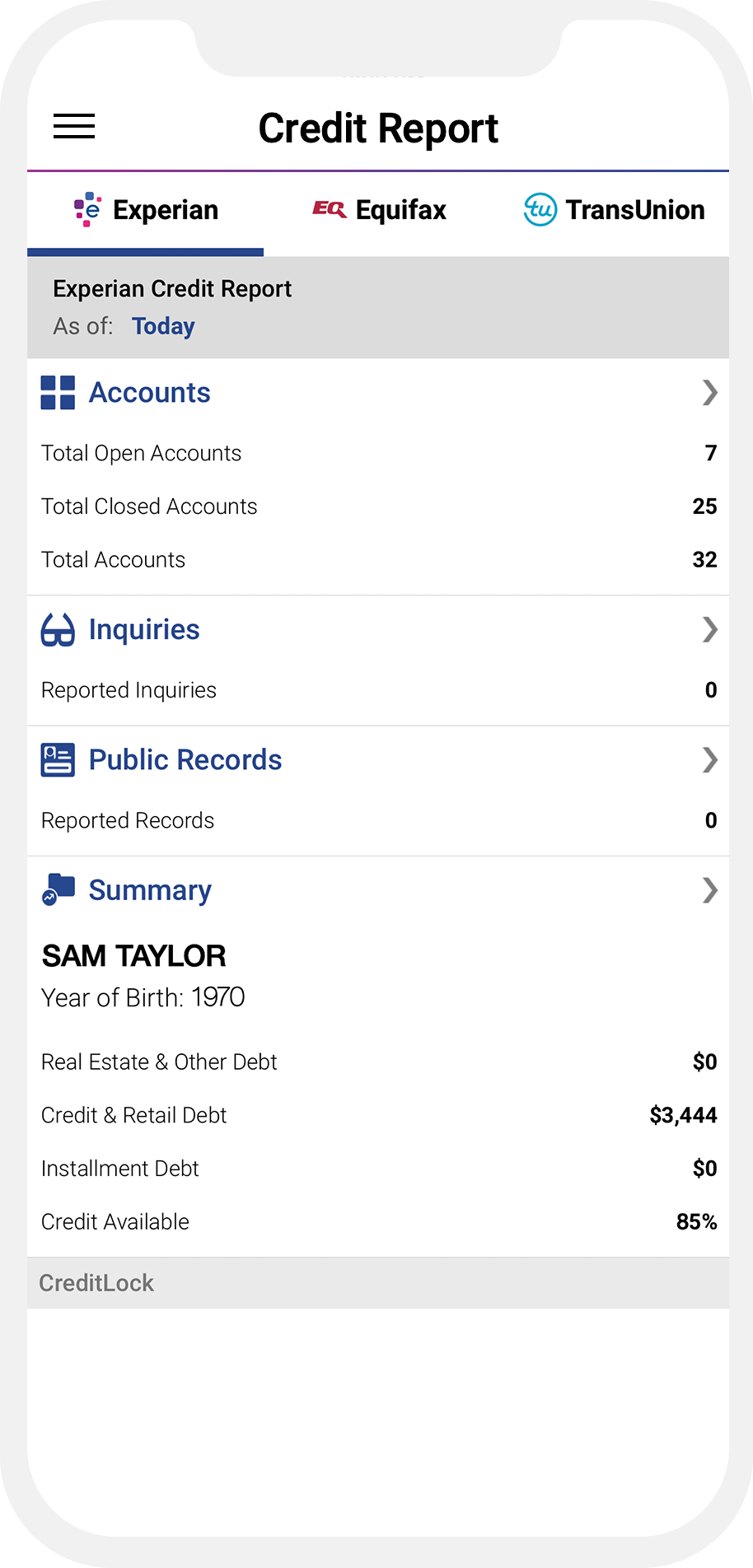

Source: ctfassets.net

Simple Steps You Can Take

- Pay your bills on time, every time. "Be punctual," they say!

- Keep your credit card balances low.

- Try to keep open the accounts you have. (Think about opening new ones after establishing good history.)

- Don't apply for too much credit at once. Don't get loans from everywhere.

- Check your report regularly. Keep an eye on how your record is looking.

What if There's a Mistake on Your Credit Report?

Mistakes happen… It's important to spot errors on your report.

How to Dispute Incorrect Information:

Source: experian.com

- Carefully read your credit report. Look for any inaccuracies.

- Gather documentation of the mistake. "Prove it," they say.

- Contact the credit bureau (Experian, Equifax, or TransUnion). Explain the mistake politely and provide evidence.

- Request a correction or removal of inaccurate information.

Questions You Might Have

Q: What happens if I have a low credit score?

A: A low score might mean it's harder to get a loan or credit card with favorable terms. (You want to work towards a better score.)

Q: How can I improve my credit score?

A: Pay your bills on time, keep your credit utilization low, don't apply for too much credit at once, keep your accounts open, and check your report regularly.

Q: How often should I check my credit report?

A: Checking your report regularly is like checking in on yourself. You can check once a year for free.

Q: What is the difference between credit reports and credit scores?

A: A credit report shows a lender all the facts about your borrowing history. A credit score is one number summarizing that history and risk. (Think of a credit report as the full report card, and the credit score as your final grade.)

Building a Strong Credit History

Building a great credit history takes time, effort, and discipline, but it’s important to your financial future. Start building your credit now!

Table: Key Credit Report Terms

| Term | Description |

|---|---|

| Credit Score | A number showing how likely you are to repay your debt, important for lenders. |

| Payment History | Your track record of paying bills on time. |

| Credit Inquiries | The number of times you've applied for credit. |

| Credit Utilization | The percentage of your available credit that you're currently using. |

| Credit Report | A detailed report of your borrowing history, checked by lenders before approving loans or credit. |