My Experian Score | Track Your Credit Progress

October 7, 2024

Your Credit Score: A Friendly Guide

Your credit score… it's a number that can seem kinda scary, but it's actually just a snapshot of how you handle borrowing money. Think of it like a report card for your financial responsibility. A good score means you're a responsible borrower, and a bad score… well, that means it might be tougher to get a loan or a credit card later. But don't worry, you can totally improve it!

What's This "Credit Score" Anyway?

Source: ctfassets.net

A credit score is a three-digit number that lenders use to predict how likely you are to pay back your debts. Higher scores mean lenders see you as a lower risk. It's like a report card for your borrowing habits. Lots of factors go into making it up, making it a pretty important part of your financial future.

Key Factors That Shape Your Score:

- Payment history: Paying bills on time is super important. Missed payments hurt your score.

- Amounts owed: How much debt you have plays a part. Having lots of credit card debt can make it look like you might have trouble paying back money.

- Length of credit history: The longer you've had accounts, the better!

- New credit: Applying for too many new credit cards or loans at once can be a red flag.

- Credit mix: Having various types of credit (like credit cards and loans) can help your score, too.

Your Credit Report: A Deep Dive

Your credit report is like a detailed biography of your borrowing habits. It shows lenders all the info on your accounts. It's basically a complete record of all the loans, credit cards, and other accounts you've ever had.

Common Sections in Your Report:

- Personal Information: Your name, address, social security number (a very important one!).

- Credit Accounts: A list of all your credit cards, loans, and any other debts.

- Payment History: This part highlights when you've paid your bills on time or if there were any late payments.

- Credit Inquiries: This section records when someone (like a lender) checks your credit.

- Public Records: Any things like bankruptcy or tax liens.

Why Does My Score Matter?

Source: mzstatic.com

Your credit score affects tons of things… It's a big deal when you want to…

- Get a loan: For a car, a house, or even a small business loan.

- Rent an apartment: Landlords might check your credit to see if you'll pay rent on time.

- Get a job: Some companies might check your credit score when considering you for a position.

- Get a cell phone: Certain providers may use it as a criteria.

- Get a credit card: It's a vital part of opening a new credit card account.

- Get a personal loan: Important for situations such as debt consolidation.

Source: krebsonsecurity.com

How Can I Improve My Score?

Improving your credit score is a marathon, not a sprint! It takes time, and there are some strategies to help…

Actions You Can Take to Boost Your Score:

- Pay your bills on time, every time! This is the most important thing.

- Keep your credit utilization low. This means use less than 30% of your available credit.

- Check your credit report regularly. Know what's in there, and that's how you stay on top of it.

- Avoid opening too many new accounts at once. Give each account a chance to build a strong history, just like in school, study before you're tested!

- Maintain a good credit mix. Have a variety of accounts (credit cards, loans).

- Don't close unused accounts. Closing accounts that you aren't using can hurt your score by shortening your history.

Credit Myths Busted!

There are a lot of rumors and myths surrounding credit scores, some of which are…

- Myth 1: Checking your credit score hurts it. This isn't true! Checking your report doesn't hurt it.

- Myth 2: You need a perfect score to be happy. Aim for a high score, but even a good score means you are on the right track.

- Myth 3: Only lenders use credit scores. No, a lot of places you want to go to, like a rental company, can use your report to know if you're a good candidate.

Questions to Ask Yourself:

- How often do I check my credit report? … (Is it enough? How could you do it more often?)

- What is my current credit utilization? … (Is it low enough to help my score?)

- Are there any errors or inaccuracies on my credit report? … (It's a good idea to find out!)

- What are my next steps? … (Are there any habits you can start to do better to increase your score?)

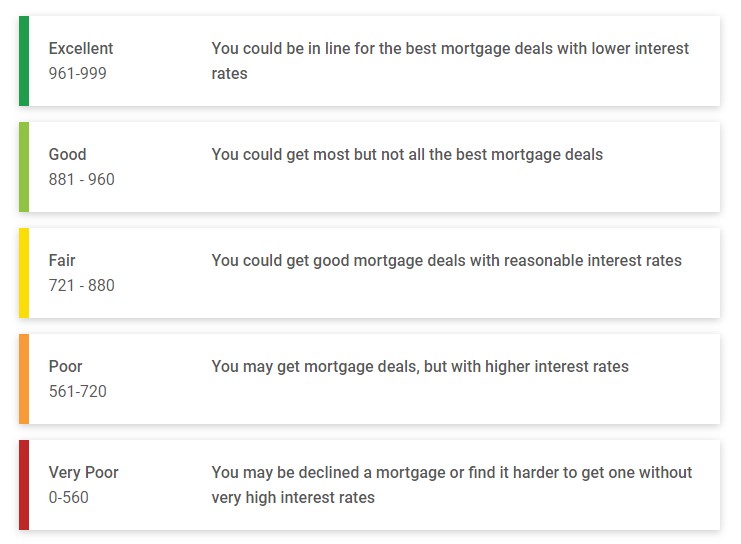

Understanding Your Credit Score:

Source: co.uk

(A Table to Help You Visualize)

| Score Range | Description |

|---|---|

| Excellent (750+) | "You're in great shape!" (This usually means you're a responsible borrower.) |

| Good (700-749) | "Good job!" (Your finances are on the right track.) |

| Fair (650-699) | "You're making progress! Keep working towards an excellent score." |

| Poor (600-649) | "Try to work on ways to improve your score. Pay your bills on time, keep credit utilization low, and ask questions for assistance." |

| Very Poor (<600) | "There's room for improvement! Focus on paying bills on time and keeping your credit utilization low." |

Taking Charge of Your Financial Future

Don't let your credit score be a mystery! By understanding what it is, how it works, and what you can do to improve it… you're taking a step toward a brighter financial future. You've got this!

"The journey of a thousand miles begins with a single step."

Remember: This information is for educational purposes only. Consult with a financial advisor for personalized guidance. Good luck!